Have you ever wondered why business growth surged dramatically in the late 19th century? This era marked a significant transformation in the economic landscape, influenced by various factors that reshaped the way industries operated.

In this article, you will discover the crucial elements that fueled this growth, including the impact of the Industrial Revolution, advancements in transportation and communication technologies, and the emergence of new financial institutions. Understanding these factors will provide valuable insights into the dynamics of modern business.

We’ll explore how these elements intertwined to create unprecedented opportunities for entrepreneurs and investors alike, ultimately setting the stage for the economic developments that followed.

The impact of the Industrial Revolution on business growth

The Industrial Revolution, which began in the late 18th century and accelerated through the 19th century, profoundly transformed the landscape of business. It marked a shift from agrarian economies to industrial powerhouses, fundamentally altering production methods and economic structures across the globe.

One significant effect was the introduction of mechanization in manufacturing. Factories began to utilize machines for production, which increased efficiency and output. For instance, the textile industry saw innovations like the spinning jenny, invented by James Hargreaves in 1764, which allowed a single worker to spin multiple spools of thread simultaneously. As a result, the production capacity soared, leading to a dramatic reduction in costs and an increase in the availability of goods.

- By 1850, British cotton production had increased from 2.5 million pounds in 1770 to over 300 million pounds.

- The introduction of steam power further revolutionized industries, enabling factories to operate machinery more efficiently.

- Railroads expanded rapidly during this period, facilitating faster transportation of goods and raw materials.

Moreover, the rise of the factory system shifted labor dynamics. Many people migrated from rural areas to urban centers in search of jobs, leading to a significant increase in the labor force. Cities like Manchester became bustling industrial hubs, growing from a population of 75,000 in 1801 to over 300,000 by 1851. This urbanization not only fueled factory growth but also created a new consumer market eager to purchase manufactured goods.

Another notable example is the rise of large corporations. Companies like Carnegie Steel and Standard Oil emerged during this time, leveraging the new technologies and economies of scale. The ability to produce goods at lower costs while maintaining high quality allowed these companies to dominate their respective markets. By the late 19th century, Andrew Carnegie’s steel production had reached over 10 million tons annually, cementing his status as a leading industrialist.

The Industrial Revolution was a catalyst for unprecedented business growth. It introduced new technologies, changed labor dynamics, and paved the way for large corporations, all of which contributed to a thriving economy in the late 19th century.

Advancements in transportation and communication technologies

The late 19th century witnessed significant advancements in both transportation and communication technologies. These innovations played a crucial role in facilitating business growth by enhancing the efficiency of trade and connectivity.

One of the most notable developments was the expansion of the railway network. By 1900, the United States boasted over 190,000 miles of track, drastically reducing the time and cost of transporting goods. This network allowed businesses to access new markets and raw materials, fostering economic expansion.

- Steamships: These vessels revolutionized maritime trade, enabling faster and more reliable shipping across oceans. For instance, the first transatlantic steamship service began in 1819, connecting Europe and America more efficiently than ever before.

- Automobiles: The introduction of the automobile in the late 1800s, particularly with the Ford Model T in 1908, transformed local distribution. Businesses could now deliver products directly to consumers without relying solely on railroads.

- Telegraph and telephone: The invention of the telegraph in the 1830s and the telephone in the 1870s allowed for instantaneous communication. This capability enabled businesses to coordinate logistics and operations across vast distances, leading to improved decision-making.

These transportation and communication advancements not only facilitated the movement of goods but also enhanced the sharing of information. For example, businesses could now respond quickly to market demands and adjust their strategies accordingly. A notable case is that of Western Union, which became a dominant player in telecommunication, providing services that helped businesses streamline their operations.

The advancements in transportation and communication during the late 19th century fundamentally altered the business landscape. Companies could expand their reach, reduce costs, and improve operational efficiency, all of which were essential for thriving in an increasingly competitive environment.

The rise of new financial institutions and investment opportunities

The late 19th century marked a significant evolution in the financial landscape, characterized by the emergence of new financial institutions and diverse investment avenues. As businesses expanded, the need for capital intensified, prompting the establishment of various financial entities.

One notable development was the formation of investment banks, which played a crucial role in facilitating capital flow. Institutions like J.P. Morgan & Co., founded in 1871, became pivotal in underwriting and issuing stocks and bonds. This not only provided businesses with necessary funding but also opened up investment opportunities for a broader public.

- Savings Banks: These institutions encouraged ordinary citizens to save, while also offering loans to local businesses.

- Insurance Companies: Companies like Prudential and MetLife began to offer financial security, allowing individuals to invest their premiums.

- Stock Exchanges: The New York Stock Exchange, established in 1817, gained prominence, providing a platform for trading shares and boosting investor confidence.

As these financial institutions proliferated, they not only enhanced liquidity in the market but also fostered a culture of investment among the general populace. For instance, stock ownership became a symbol of prosperity, with many Americans participating in the stock market for the first time. By 1900, the number of stockholders in the United States had surged to over 1.5 million.

The rise of new financial instruments also contributed to this growth. The introduction of railroad bonds and other securities provided viable investment options. Investors were drawn to the potential high returns from these investments, as railroads became the backbone of the economy, facilitating goods movement and commerce expansion.

Moreover, the financial boom was further fueled by the availability of credit. As banks began to offer loans with relatively low interest rates, businesses could expand operations without the immediate need for large capital. This accessibility to credit played a vital role in the rapid growth of industries, including manufacturing and agriculture.

The role of government policies and regulations

The late 19th century saw a pivotal shift in the way governments approached economic activities and business operations. A combination of laissez-faire policies and regulatory frameworks created an environment conducive to business growth. Governments began to recognize the importance of a free market, allowing entrepreneurs to innovate and expand.

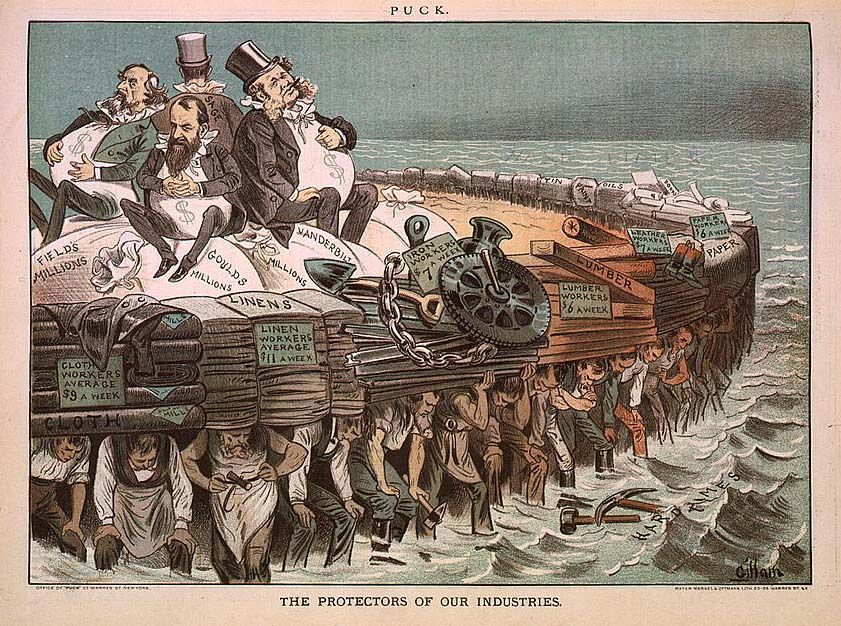

One significant aspect of government involvement was the establishment of tariffs and trade policies. For instance, the McKinley Tariff of 1890 raised duties on imported goods, which aimed to protect domestic industries from foreign competition. This policy encouraged local production and increased investment in manufacturing sectors.

- Railroad Regulation: The Interstate Commerce Act of 1887 was a landmark legislation that aimed to regulate the railroad industry. It sought to ensure fair rates and eliminate monopolistic practices.

- Banking Reforms: The National Banking Act of 1863 established a system of national banks and created a uniform currency, fostering stability in the financial system.

- Labor Laws: As labor movements gained momentum, governments began to implement regulations to protect workers. This included laws addressing working conditions, child labor, and wages.

Moreover, government land grants and subsidies significantly aided the expansion of industries, particularly in the railroad sector. The Pacific Railway Act of 1862 facilitated the construction of the transcontinental railroad, which not only connected the East and West coasts but also opened up new markets for goods and services.

Another example of government support can be seen in the rise of patent laws which encouraged innovation. The Patent Act of 1870 streamlined the patent process, providing inventors with legal protection for their creations. This legal framework empowered entrepreneurs, leading to a surge in inventions and business ventures.

Government policies and regulations during the late 19th century played a critical role in shaping the business landscape. By implementing protective tariffs, regulatory frameworks, and supportive legislation, governments fostered an environment ripe for innovation and growth, ultimately contributing to the economic expansion of the era.

Expansion of domestic and international markets

The late 19th century was marked by a remarkable expansion of both domestic and international markets. This growth was driven by several interrelated factors, including increased industrial production, advancements in transportation, and a burgeoning consumer base. The United States transitioned from a predominantly agrarian economy to an industrial powerhouse, leading to a surge in manufactured goods.

By 1900, the U.S. produced about one-third of the world’s industrial output, a monumental shift from just a few decades earlier. This rapid industrialization created a demand for raw materials and new markets for finished products, prompting businesses to explore opportunities beyond national borders.

- Rise of Exports: U.S. exports rose from $1.4 billion in 1870 to $3.2 billion by 1900.

- New Markets: The opening of markets in Asia and Latin America provided American businesses with opportunities for expansion.

- Foreign Investments: American investments in infrastructure abroad, such as railroads in Central America, facilitated trade.

One of the most notable examples of international market expansion during this period was the Spanish-American War in 1898. The war resulted in the U.S. acquiring territories like Puerto Rico, Guam, and the Philippines. This acquisition allowed American businesses to tap into new markets and resources, significantly contributing to economic growth.

Domestically, the expansion of railroads played a critical role in linking producers to consumers. By 1900, the U.S. had over 193,000 miles of railroad track, drastically reducing transportation costs and time. This infrastructure allowed for the efficient distribution of goods across the country, which in turn fueled regional market development.

Moreover, urbanization during this period created a concentration of consumers in cities. The growing middle class, with increased disposable income, demanded a wider variety of goods, which further stimulated production and market expansion. By 1900, approximately 40% of Americans lived in urban areas, up from just 20% in 1870, illustrating the shift in economic and market dynamics.

The influence of entrepreneurship and innovation

The late 19th century was a period of remarkable entrepreneurial spirit and innovation that significantly influenced business growth. Entrepreneurs such as Andrew Carnegie and John D. Rockefeller revolutionized industries through their visionary ideas and business practices. Carnegie, for instance, transformed the steel industry by implementing new production methods, which drastically reduced costs and increased output.

Moreover, the rise of inventions during this period played a crucial role in economic expansion. The telephone, invented by Alexander Graham Bell in 1876, and the electric light bulb, developed by Thomas Edison in 1879, enhanced communication and productivity. These innovations not only improved daily life but also created new markets and business opportunities.

- Andrew Carnegie: Established the Carnegie Steel Company, which became the largest and most profitable steel company in the world.

- John D. Rockefeller: Founded Standard Oil, dominating the oil industry and setting standards for corporate practices.

- Thomas Edison: Created General Electric, one of the largest and diversified industrial corporations in the world.

The impact of innovation extended beyond individual entrepreneurs. The late 19th century also saw the rise of industrial research laboratories, which facilitated the development of new products and processes. Notable companies like General Electric and Westinghouse invested heavily in research and development, leading to technological advancements that fueled further industrial growth.

Additionally, the establishment of patent laws encouraged inventors to protect their creations. The U.S. Patent Office, founded in 1790, played a vital role in safeguarding intellectual property, promoting a culture of innovation. By the end of the century, over 1 million patents had been issued, showcasing the creativity and ingenuity of American inventors.

This era’s entrepreneurial drive and innovation not only transformed existing industries but also laid the groundwork for future advancements. The synergy between entrepreneurship and technological progress fostered a dynamic economic environment, paving the way for the 20th century’s economic boom.

Changes in labor force and workforce organization

The late 19th century experienced profound changes in the labor force and how it was organized, which significantly contributed to business growth. The transition from agrarian economies to industrialized ones created a demand for a different type of workforce. This shift led to notable developments, including:

- Increased urbanization: As factories emerged, people flocked to cities for work. By 1900, over 40% of the U.S. population lived in urban areas, compared to just 20% in 1860.

- Rise of wage labor: The traditional system of self-employment began to decline, replaced by wage labor. This created a more stable workforce that could be hired and laid off according to the economic needs of businesses.

- Formation of labor unions: Workers began organizing to demand better wages and working conditions. By the 1880s, notable unions like the Knights of Labor had emerged, advocating for the rights of workers.

Innovations in management and organization also played a crucial role in optimizing labor productivity. The introduction of assembly line techniques in factories, notably by figures like Henry Ford in the early 20th century, revolutionized production processes. However, the groundwork for such innovations was laid in the late 19th century, as companies sought to maximize efficiency.

For example, the American Steel Industry saw significant advancements during this time. Under the leadership of Andrew Carnegie, the steel mills adopted systematic approaches to workforce management, emphasizing task specialization. This not only improved output but also set a precedent for future industrial practices.

- Skilled vs. unskilled labor: The demand for skilled labor increased as industries grew. Skilled workers were often better compensated, while unskilled labor remained abundant and cheap.

- Women in the workforce: The late 19th century marked the entry of women into various industries, particularly textiles and clerical work. By 1900, women constituted nearly 20% of the workforce in the U.S.

- Child labor: Unfortunately, child labor was prevalent, with many children working in dangerous conditions. This prompted public outcry and eventually led to reforms in labor laws.

These transformations in the labor force and workforce organization not only enhanced productivity but also laid the foundation for the modern business environment. As businesses adapted to these changes, they were better positioned for growth, setting the stage for the economic boom of the early 20th century.

The development of large corporations and trusts

The late 19th century witnessed the emergence of large corporations and trusts, which fundamentally changed the landscape of American business. These entities allowed for the consolidation of resources and capital, leading to increased efficiency and market dominance. Prominent figures such as John D. Rockefeller and Andrew Carnegie exemplified this trend, creating vast empires in the oil and steel industries, respectively.

Corporations like Standard Oil and U.S. Steel utilized innovative strategies to minimize competition and maximize profits. They achieved this through vertical and horizontal integration, which enabled them to control every aspect of production and distribution. For instance, by acquiring suppliers and competitors, these corporations could dictate prices and stabilize their markets.

- Vertical Integration: Owning the supply chain from raw materials to finished products.

- Horizontal Integration: Acquiring or merging with competitors to reduce competition.

- Trusts: Legal arrangements where several companies would act as a single entity to control prices.

By 1900, large corporations dominated numerous industries. For example, Standard Oil controlled over 90% of the U.S. oil refining market, while U.S. Steel became the first billion-dollar corporation in American history. These monopolistic practices led to public outcry and ultimately prompted regulatory measures, such as the Sherman Antitrust Act of 1890, aimed at curbing the power of these large entities.

The rise of corporations also transformed the labor market. As businesses grew, they required a more structured workforce, leading to the development of organized labor movements. Workers began to unionize to advocate for better wages and working conditions, challenging the power of corporations. The pull between corporate interests and labor rights became a defining feature of the late 19th century.

The development of large corporations and trusts during this period was a double-edged sword. While they contributed to economic growth and efficiency, they also raised significant ethical and social concerns that shaped the future of American business.

Urbanization and its effect on consumer demand

The late 19th century saw an unprecedented wave of urbanization, with cities expanding rapidly. By 1900, approximately 40% of the U.S. population lived in urban areas, compared to just 20% in 1860. This shift significantly altered consumer behavior and demand.

As more individuals migrated to cities in search of jobs, they created a dense population of consumers with varied needs. Urban centers became hubs for commerce and trade, leading to increased demand for goods and services. This resulted in the growth of retail businesses and the introduction of new products to meet the diverse wants of urban consumers.

- Increased accessibility: Urbanization made it easier for businesses to reach consumers, facilitating the establishment of department stores like Macy’s in New York City, which opened its doors in 1858.

- Consumer variety: The influx of people from different regions introduced a mix of cultural preferences, demanding a wider range of products.

- Transportation advancements: Innovations such as the expansion of railroads and streetcars allowed for quicker delivery of goods, meeting consumer demand efficiently.

Additionally, urbanization led to the rise of advertising as businesses sought to capture the attention of city dwellers. Companies began using newspapers and posters to promote their products, which became essential for reaching the growing consumer base. For instance, the introduction of mass marketing techniques in the late 1800s laid the groundwork for a consumer culture centered around brand recognition.

One notable example is the rise of mail-order catalogs, like those from Sears, Roebuck and Co., which allowed rural consumers access to products previously available only in urban markets. Founded in 1893, Sears revolutionized shopping by offering a wide array of goods, from clothing to household items, shipped directly to consumers.

Urbanization transformed the landscape of consumer demand in the late 19th century. The combination of a growing urban population, improved transportation, and targeted marketing resulted in a dynamic market environment that fostered business growth and innovation.

Frequently Asked Questions

What factors contributed to the growth of businesses in the late 19th century?

Key factors included industrialization, advancements in technology, and the rise of urbanization. These elements created a favorable environment for businesses to expand and innovate, leading to increased production and consumer demand.

How did urbanization affect consumer behavior?

Urbanization led to a significant shift in consumer behavior, as more people moved to cities and sought diverse goods and services. This increased demand prompted businesses to adapt their offerings and expand their operations to meet the needs of a growing urban population.

What role did large corporations play in business growth?

Large corporations emerged as powerful entities that dominated the market. They facilitated economies of scale, enabling more efficient production methods and lower costs, which were crucial for driving business growth during this period.

How did changes in the labor force impact businesses?

Changes in the labor force, including a shift towards organized labor and improved workforce management, allowed businesses to operate more efficiently. This led to increased productivity and innovation, which were essential for growth in a competitive marketplace.

What was the impact of technological advancements on business growth?

Technological advancements, such as the introduction of machinery and improved transportation, revolutionized production processes. These innovations enabled businesses to increase output and reduce costs, driving significant growth during the late 19th century.

Conclusion

The late 19th century was marked by significant transformations in the labor force, the rise of large corporations and trusts, and rapid urbanization. These factors collectively fueled business growth by enhancing efficiency, consolidating markets, and increasing consumer demand in expanding urban areas. By understanding these historical trends, readers can gain insights into modern business practices, particularly in workforce management and market strategies. Recognizing the impact of urbanization and corporate structures can lead to more effective decision-making in today’s business environment. To explore these concepts further, consider researching current trends in workforce organization and urban consumer behavior. This knowledge can empower you to adapt and thrive in the evolving business landscape.